Lithium-iron phosphate (LFP) battery chemistry has officially overtaken traditional nickel-based packs to become the most widely deployed electric vehicle battery technology globally in 2025. This significant shift, driven largely by China’s manufacturing dominance and the cost-effectiveness of LFP technology, marks a new era in the electric vehicle battery landscape.

LFP Surges Ahead in 2025

According to research firm RhoMotion, LFP experienced the fastest growth among battery chemistries in 2025, with demand increasing by an impressive 48%. This surge has propelled LFP past nickel-manganese-cobalt (NMC) batteries, which previously benefited from a mature supply chain and higher energy density crucial for achieving desirable EV driving ranges.

The Advantages of LFP

For years, automakers favored NMC batteries due to their established infrastructure and performance. However, the mining of nickel and cobalt is costly, environmentally intensive, and often linked to controversial supply chains, including reports of labor and human rights violations, particularly in the Democratic Republic of Congo. In contrast, LFP batteries offer a more affordable, environmentally conscious, and ethically sourced alternative.

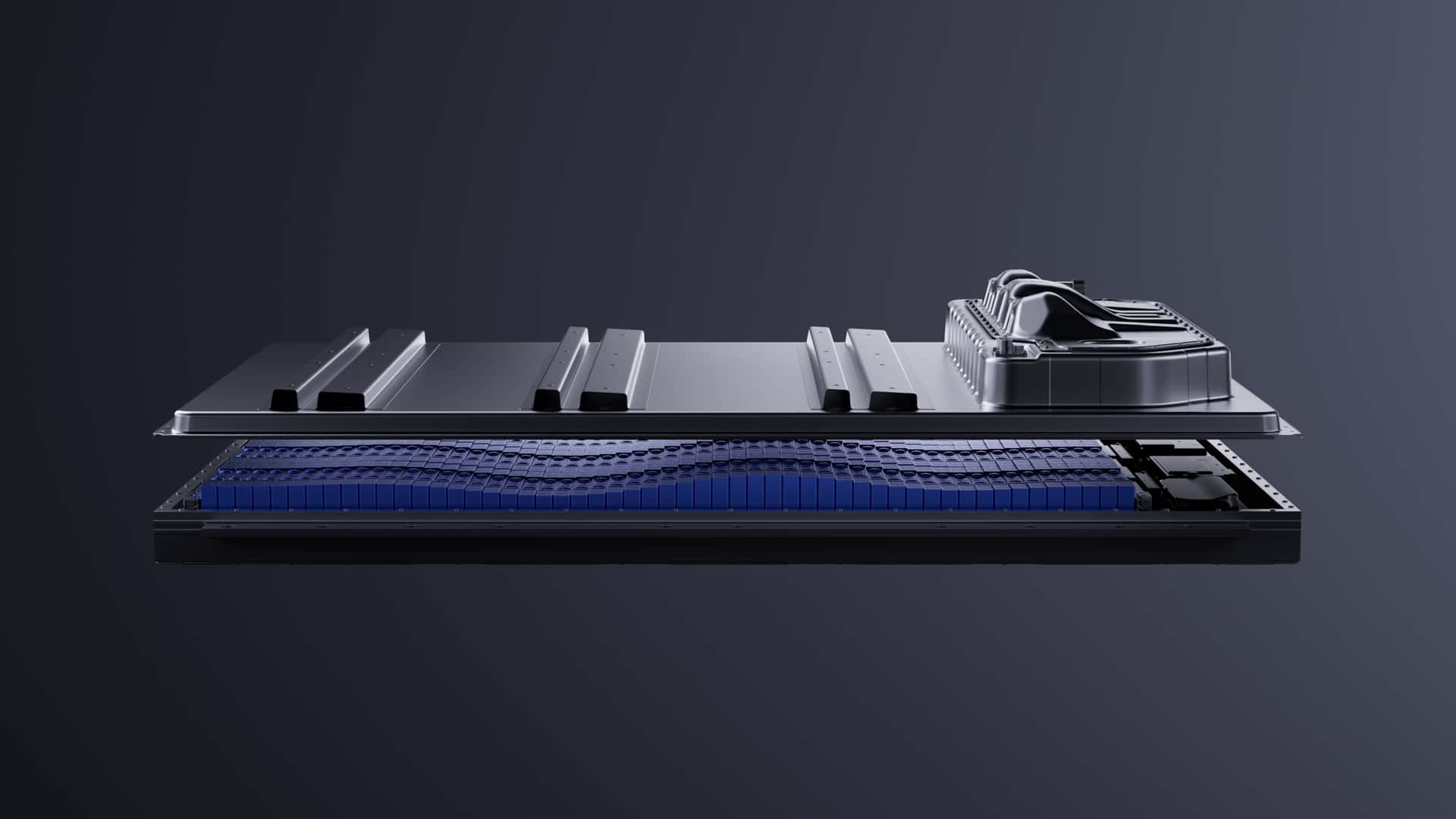

The gap in energy density between LFP and NMC batteries is also narrowing. Innovations such as cell-to-pack and cell-to-chassis designs allow for more battery cells to be integrated into the same physical space. Furthermore, advancements in anode and cathode materials are steadily improving the performance of LFP batteries, making them increasingly competitive.

China’s Leading Role

China has been at the forefront of the LFP revolution, with Chinese automakers and battery manufacturers spearheading the transition. In the period between January and November 2025, over 80% of electric vehicles sold in China were equipped with LFP batteries, underscoring the country’s commitment to this technology. This dominance is now extending to global markets.

Global Expansion and Regional Trends

Europe and Asia (excluding China) accounted for approximately 75% of the global LFP growth in 2025. This expansion is largely attributed to the increasing influx of Chinese EVs into international markets. In Europe, Chinese automakers captured a record 12.8% of the EV market in November 2025, more than doubling their market share from the previous year, according to data from Dataforce cited by Bloomberg. Leading Chinese brands such as BYD, Leapmotor, and Chery have reported significant growth in the region.

CATL, a Chinese battery giant, is a dominant force in the LFP market, with its battery cells found in roughly one-third of all EVs sold globally in 2025. To support this growth and mitigate potential tariffs, Chinese battery manufacturers are establishing local LFP production facilities in Europe. BYD and CATL are constructing battery plants in Hungary, while CATL already operates a facility in Germany and plans another in Spain in partnership with Stellantis.

North America’s LFP Landscape

North America stands as an exception, with LFP deployments seeing a decline in 2025. The U.S. has implemented tariffs and strict sourcing requirements, notably through the Biden-era Inflation Reduction Act, which has effectively restricted the import of Chinese-made batteries. Consequently, only a limited number of LFP-equipped EVs are available in the U.S. market.

While Tesla briefly offered LFP batteries on base Model 3 vehicles in the U.S., tariffs led to the discontinuation of that trim. Rivian and Ford continue to utilize LFP packs for base models of their R1S, R1T, and Mustang Mach-E. However, an anticipated resurgence of LFP in the U.S. is expected, fueled by more affordable EV options like the new Chevrolet Bolt and Ford’s upcoming $30,000 electric truck.

Future Outlook for LFP in the U.S.

The growth trajectory for LFP in the U.S. is expected to differ from that in Europe and China. A significant portion of this future momentum is anticipated to stem from domestic production of battery energy storage systems (BESS), rather than solely from passenger EVs. Following the expiration of the $7,500 federal tax credit, several U.S. battery manufacturers, including LG Energy Solution, Tesla, and SK On, have reallocated their battery manufacturing capacity towards the BESS market, which is experiencing faster growth than the EV sector.